Mortgage application checklist for expats (2026 Update)

Dutch mortgage rules may change from year to year, but the main documents expats need stay almost the same. In 2026, you need to provide clear proof of your income, employment, residency, and financial stability. Start gathering these documents early to speed up and simplify your mortgage approval process.

To get a mortgage in the Netherlands, you need to demonstrate your ability to make the monthly payments. This means providing documents about your income, savings, debts, and the property you want to buy. If you are applying with someone else, both of you must submit your own documents. In this blog article, our mortgage advisor Robin from OHAO overviews the documents required to get your mortgage approved in the Netherlands.

What do you need for your first mortgage consultation?

If you to get the most from your first call with our mortgage advisor , it helps to gather some key documents ahead of time. The most important is your latest salary slip or, if needed, your employer’s statement. This lets the advisor check your finances and give you a good idea of how much you can borrow in the Netherlands.

If you intend to purchase a property together with a partner or family member, they should also have their latest salary at the meeting.

Having both documents helps the advisor give you a clear, accurate picture of your combined borrowing capacity, so you start the process with realistic expectations.

1. If you are employed

For employees, the mortgage process is usually the simplest because your income is steady and predictable. Mortgage lenders use your salary documents to check your finances and decide how much you can borrow.

You need to provide documents that show your financial situation and demonstrate your ability to pay the mortgage. These help the lender determine your loan-to-income (LTI) ratio, which determines how much you can borrow.

Required documents

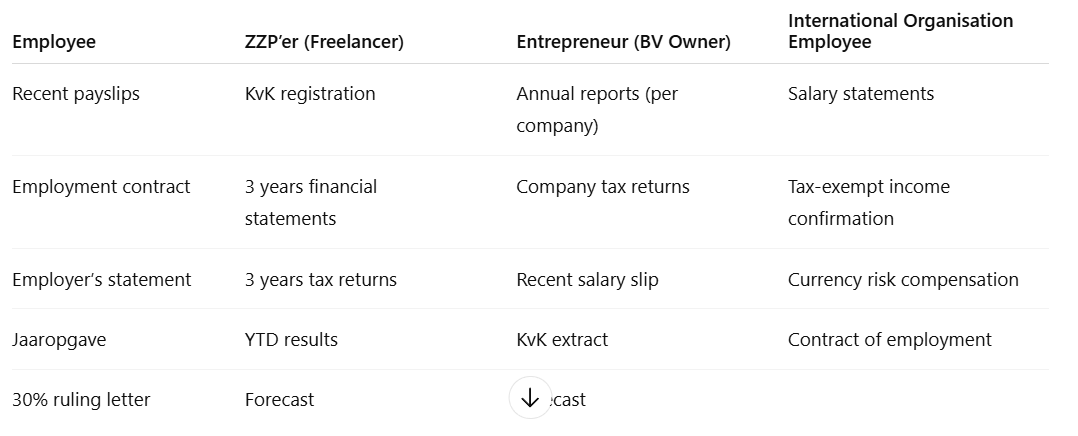

To apply for a Dutch mortgage, you should submit your recent payslips, your employment contract, and an employer’s statement (werkgeversverklaring).

The employer’s statement is especially important because it confirms your salary, contract type, fixed allowances, and whether your employer expects to extend your contract in the future.

You also need to provide your annual income statement (jaaropgave) and your most recent income tax return. If you receive the 30% ruling, include the confirmation letter to ensure your tax-free income is factored in correctly.

If you have a temporary or fixed-term Contract

You can still get a mortgage even if you have a temporary contract. If your employer gives you a letter of intent to extend your contract, lenders may treat your job as permanent. This can let you borrow more.

Some mortgage lenders are flexible even without a letter of intent if you have worked in the same field for a long time or have good job prospects.

2. If you are a freelancer (ZZP’er)

Freelancers face different mortgage requirements because their income can fluctuate throughout the year. Mortgage lenders need to see that your business generates stable, reliable profit. Instead of looking at a fixed monthly salary, they evaluate your income based on your historical business performance.

How lenders assess freelancers

To qualify for a mortgage as a ZZP’er, you generally need:

At least 12 months of business activity, and

A valid registration with the Chamber of Commerce (KvK)

Dutcg mortgage lenders usually want to see three full years of financial history to get a clear picture of your income. They often base your borrowing limit on your average net profit over those years. If your income has gone up, some lenders may use your most recent year instead.

If your business is less than three years old, you can still apply. Many lenders now have options for freelancers with a short business history. Sometimes, they may also consider your previous job income, especially if your freelance work is in the same field.

Required documents

As a freelancer, you must submit:

Annual financial statements (up to 3 years)

Tax returns (up to 3 years)

Year-to-date business results

A business forecast for the remainder of the year

(If applicable) a shareholder agreement

3. If you are an entrepreneur (business owner)

Entrepreneurs (BV) with one or more companies face requirements similar to those of freelancers but often have more extensive documentation. Mortgage lenders must assess not only your personal income but also the health and stability of each business you own.

How lenders assess entrepreneurs

You mainly need to provide financial statements (annual reports) for each company you own from the past three years. These let lenders check company assets, debts, profits, and overall financial strength. If your company is younger than three years, provide what you have.

Dutch mortgage lenders also want to understand your role in the business—whether you pay yourself a salary, how much equity you hold, and how dependent the company is on your involvement.

Required documents

For each company you own, lenders require:

Annual financial statements (up to 3 years)

Company tax returns (up to 3 years)

A recent salary slip (if you pay yourself a salary)

Year-to-date business results

KvK registration extract

An organisation chart

A financial forecast for the remainder of the year

4. If you work for an international organisation

Income from international organizations is handled differently from regular Dutch employment, and each lender has its own rules. For details about a specific lender, please contact our mortgage advisors.

Income paid in foreign currency

If you are paid in a currency other than euros, lenders will convert your salary using the current exchange rate. Many international organizations offer currency adjustment or risk compensation, and lenders consider these because they help keep your income steady. This makes your finances look more predictable.

Tax-exempt income

If you work for organizations like Europol, OPCW, ICC, ESA, or UN agencies, your income may be partly or fully exempt from Dutch income tax. Lenders look at your net income, so this tax benefit can increase how much you can borrow. Sometimes, tax-exempt income gives you more room in affordability checks than regular Dutch-taxed income.

Employment stability

International organisations are usually seen as very stable employers. Long-term contracts, clear job structures, and strong institutional backing make income from these jobs dependable. This stability can help your mortgage application.

Differences between lenders

Policies differ significantly. Some mortgage lenders have strict rules about foreign currency or tax-exempt income, while others specialize in expats and international-organisation employees and may offer more flexible mortgage terms.

5. If you have a temporary or fixed-term contract

Applicants with temporary contracts can still qualify for a mortgage. If you have a temporary contract, you can still get a mortgage, but lenders need to be sure your income will continue. A letter of intent from your employer states they plan to extend your contract. With this letter, many lenders treat your job as permanent.

If you do not have a letter of intent, some lenders may still approve your application if:

You have been working in the same profession for a long period

Your employer has a strong financial position

You can show a consistent income history.

If you want to check whether you qualify for a mortgage and ensure you have all the right documents in place, our experienced mortgage advisors are here to help. Whether you are buying your first home, upgrading to your second, or considering refinancing, we guide you through each step with clarity and confidence.

Our happy clients

We focus on delivering great results — and our clients' feedback tells the rest of the story.