Whether you buy a home alone or with someone else can make a €100,000+ difference in your maximum mortgage. If you are weighing up your options — solo, with a partner, or even with a friend or a family member — this article is written by our mortgage advisor Toni at OHAO and guides you on how much you can borrow in 2026.

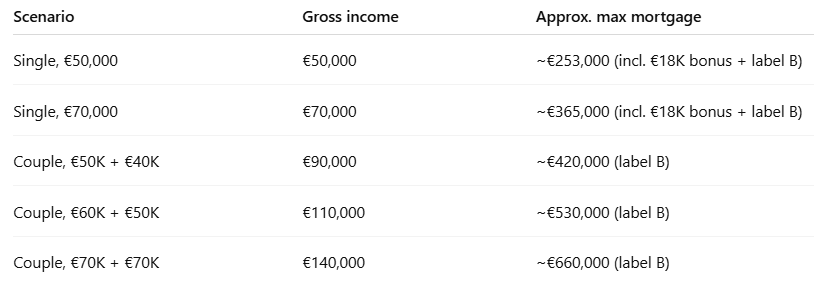

In short: single buyers use only their own income but get an extra €18,000 borrowing allowance (income ≥ €28,000). Couples benefit from both incomes at 100%. A single earner at €50,000 might borrow ~€253,000; a couple earning €50K + €40K could reach ~€420,000, which can be a good start if you want to enter the Dutch housing market.

What income counts when you buy alone?

When you apply on a single income, the lender builds your toetsinkomen (qualifying income) from several components, not just your base salary. Understanding exactly what is included helps you maximise your borrowing power. For accurate mortgage calculations, please contact our mortgage advisors.

Employed buyers — what lenders include

Base salary — your gross annual salary as stated in your employment contract

Holiday allowance (vakantiegeld) — the standard 8% is automatically included

13th month / end-of-year bonus — included in full if it is contractually guaranteed and unconditional

Commission — personal, performance-based commission is usually averaged over the past 12 months and must appear on the employer statement (if applicable)

Bonus — team or company-wide bonuses are typically averaged over the past 3 consecutive years; if you have less than 3 years of history, some lenders may accept the last 12 months

Structural overtime and irregular hours allowance — included if your employer confirms they are ongoing and if this is applicable in your case

Confirmed future salary increase — if a raise is unconditional and takes effect within 6 months, most lenders are willing to use the higher figure

For a full breakdown of how lenders convert these components into your maximum mortgage, see how the maximum mortgage is calculated in the Netherlands.

Self-employed (ZZP) buyers — a different calculation

Mortgage lenders and banks look at your average net profit from the past 1 to 3 years, based on your tax returns and annual accounts. The more years you can show, the stronger your case will be.

When reviewing your application, lenders pay close attention to whether your profits are going up, staying the same, or going down; what industry you work in and how risky it is; how steady your cash flow is; and if you used to work as an employee in the same field, as it helps show you have experience and stability.

Most banks now accept applications after just 12 months of self-employment, especially with an NHG-backed mortgage. However it all depens son your business legal status.

If you have your own business, OHAO mortgage advisors can already start preparing your mortgage application even if you do not yet have 12 months of business history. We can review your situation, explain which documents you will need, and help you prepare everything in advance. As soon as you reach the 12-month mark, the mortgage application can be submitted immediately.

The single-buyer bonus

If you are buying a home on your own and your gross annual income is at least €28,000, you get an extra €18,000 added to your borrowing limit. This bonus is meant to reflect the fact that single-person households usually have lower living costs, so you can put more toward your mortgage. You get this boost whether you are employed or self-employed.

Family help: gifts and family mortgages

Buying solo and your mortgage max just does not stretch to that dream home? Family can step in to help close the gap. There are two main ways they can do this, but each comes with its own rules and tax implications.

Donation (schenking)

Parents or other family members can make a financial gift toward your home purchase. In 2026, the annual tax-free gift exemption from parents to a child is €6,908.

In addition, there is a one-time increased gift tax exemption of €33,129 for children aged 18–40. This exemption can be used freely, including for purchasing a home. This one-time exemption can only be claimed once in a lifetime, regardless of when it was last used. Please note: for expats whose parents live abroad, there is no limitations on the amount.

Important note for Dutch nationals: the large tax-free gift specifically earmarked for home purchases (the "jubelton") was abolished from 2024. The one-time increased exemption of €33,129 still exists, but it is a general exemption — not exclusively for housing. Any amount above the applicable exemption is taxed at 10% on the first €158,669 and 20% above that (for parent-to-child gifts).

A donation does not affect your parents' borrowing capacity at their own bank, making it a clean way to help without creating new liabilities.

Family mortgage (familiehypotheek)

A family mortgage is a loan from your parents (or other family members) to help finance part of your home purchase, often alongside a regular bank mortgage. It is increasingly common, but the Dutch tax authority (Belastingdienst) has strict rules for the interest to remain tax-deductible:

The loan must be recorded in writing — a verbal agreement is not enough

The interest rate must be comparable to market rates that a bank would charge under similar conditions — too low and the tax authority may treat the difference as a gift; too high and the excess interest is not deductible

Repayments must be made monthly via actual bank transfers — a "paper loan" where no money changes hands is not permitted

The loan must be fully repaid within 30 years using an annuity or linear repayment structure

The agreement must specify what happens if one party passes away or the home is sold

One common arrangement is for parents to make a separate annual donation roughly equal to the interest their child pays on the family mortgage. This is allowed, but the donation must not be contractually linked to the interest payments. There must be no causal connection — the donation should happen at a different time of year and should not be documented in the same agreement as the loan. If the tax authority considers the donation and the interest payments to be connected, the interest deduction may be disqualified.

Do you want to explore how to combine a traditional mortagge with a family mortgage? Book a free consultation with one of our advisors at OHAO.

How does buying together change things?

When you buy with a partner, both incomes are counted at 100% in the mortgage calculation (fully included since 2023, up from 90% previously). The single-buyer bonus does not apply, but the combined income almost always results in a much higher maximum.

Disclaimer: example figures based on a 30-year annuity mortgage, ~3.6% interest rate (10-year fixed), no debts, energy label B. These calculations are illustrative only and individual results may vary.

Disclaimer: example figures based on a 30-year annuity mortgage, ~3.6% interest rate (10-year fixed), no debts, energy label B. These calculations are illustrative only and individual results may vary.

Can I buy with a friend, family member, or colleague?

Yes — there is no restriction on the relationship between joint mortgage applicants in the Netherlands. You can buy with a partner, friend, sibling, parent, or colleague. This is a favourable choice for single buyers who cannot afford a home on one income.

The mechanics are the same as buying with a partner: you become each other's fiscal partners and are jointly and severally liable for the full mortgage. If one person cannot pay, the other is responsible for the entire amount. A precise legal agreement covering payment responsibilities, what happens if someone wants to sell, and how equity is divided is essential. A notary can help you prepare this.

When is it better to apply alone?

Buying together is not always the best move. There are situations where applying solo actually produces a higher maximum mortgage or is strategically smarter.

Partner with low or no income: If your partner earns very little, their income may not substantially increase the maximum, and you lose the €18,000 single-buyer bonus. A mortgage advisor can run both scenarios and show you which is higher.

Partner with significant debts: If one partner has BKR-registered loans, DUO student debt, or other obligations, those debts reduce the joint maximum. Sometimes the combined income still outweighs the debt impact, but not always. Please contact our mortgage advisors for financial advice.

One partner on a temporary contract: If one has a permanent contract and the other has a temporary one without an intentieverklaring, the temporary income may not be fully counted. Check our mortgage application requirements to see what each partner needs.

Single expats with the 30% ruling: Your borrowing power gets a boost — the tax-free portion increases your effective income, and you qualify for the €18,000 bonus. This combination can make buying alone more practical than many expats expect. If your salary is paid in a foreign currency, see our guide on mortgage with foreign income.

Top frequently asked questions by expats

How much more can I borrow with a partner?

You chances of affording a more bigger house increases. Couples on €90,000 combined typically reach €400,000–€420,000 in mortgage capacity, while a single person earning €50,000 usually tops out around €253,000 once you factor in the single-buyer bonus.

What is the eenpersoonsopslag in 2026?

That is the extra €18,000 single buyers get on top if they are earning at least €28,000 in gross income. It is there because living costs are genuinely lower when you are on your own.

Can I buy a home with a friend?

Yes. Lenders do not care about the type of relationship — you are just jointly responsible for the full mortgage. Get a watertight legal agreement, though.

All calculation examples are for illustrative purposes only and do not constitute financial advice. For more information, please contact our mortgage advisors for a free, no-obligation consultation.

Our happy clients

We focus on delivering great results — and our clients' feedback tells the rest of the story.