After the Dutch government introduced stricter sustainability standards in 2024, energy efficiency became a much bigger factor in the housing market. To calculate the maximum mortgage in the Netherlands, the property's energy label is taken into account. This will remain unchanged in 2026; however, some allowances will decrease.

Read this blog article, written by Bart, our mortgage advisor at OHAO, to understand how much you can borrow in 2026 based on your home's energy label.

How does it work, and why was it introduced?

The new calculation method was introduced after a sharp rise in energy prices, leaving many households under financial pressure. To prevent this from happening again, lenders now adjust your borrowing capacity based on a home’s energy label:

Homes with a better energy label are cheaper to heat and maintain, leaving more room in your monthly budget — which means you can borrow more.

Homes with poor insulation and high energy costs reduce your financial flexibility, so lenders lower the maximum mortgage you can obtain.

Additional borrowing capacity in 2026: what is changing?

In 2026, buyers of very energy-efficient homes will get slightly less extra borrowing space. For A+++ homes, the allowance drops from €30,000 to €25,000, and for A++++ homes, it decreases from €50,000 to €40,000. This change mainly reflects the reduced financial benefits of solar panels as feed-in costs rise and the net-metering scheme ends in 2027.

Additional borrowing for buying an energy-efficient home (2026)

The more energy-efficient your home, the more you may borrow on top of your standard maximum. In 2026, your energy label determines the following:

Energy label | 2026 |

E, F, G | €0 |

C, D | €5,000 |

A, B | €10,000 |

A+, A++ | €20,000 |

A++++ | €30,000 |

A++++ (with performance guarantee) | €40,000 |

How much extra can you borrow for sustainability upgrades in 2026?

If your home has a lower energy rating, you may borrow extra specifically for upgrades such as insulation, heat pumps, solar panels, or HR++ glass.

Energy label | 2026 |

E, F, G | €20,000 |

C, D | €15,000 |

A, B, A+, A++ | €10,000 |

A+++ | €0 |

A++++ | €0 |

Why €0 for A+++ and A++++?

These homes are already extremely efficient, so there’s little left to upgrade that would meaningfully reduce energy use.

How does this work in real life?

Let’s assume you are buying a property valued at €390,000 with an energy label B.

Your situation:

Your income allows a maximum mortgage of €375,000

The home’s B label gives you €10,000 extra borrowing space.

Max amount based on income | €375,000 |

Extra borrowing for label B | + €10,000 |

New theoretical maximum | €385,000 |

Appraised home value | €390,000 |

Final mortgage | €385,000 |

Reminder: you can never borrow more than the home’s appraised value — even if the energy label allows additional borrowing because you can only get 100%loan to value.

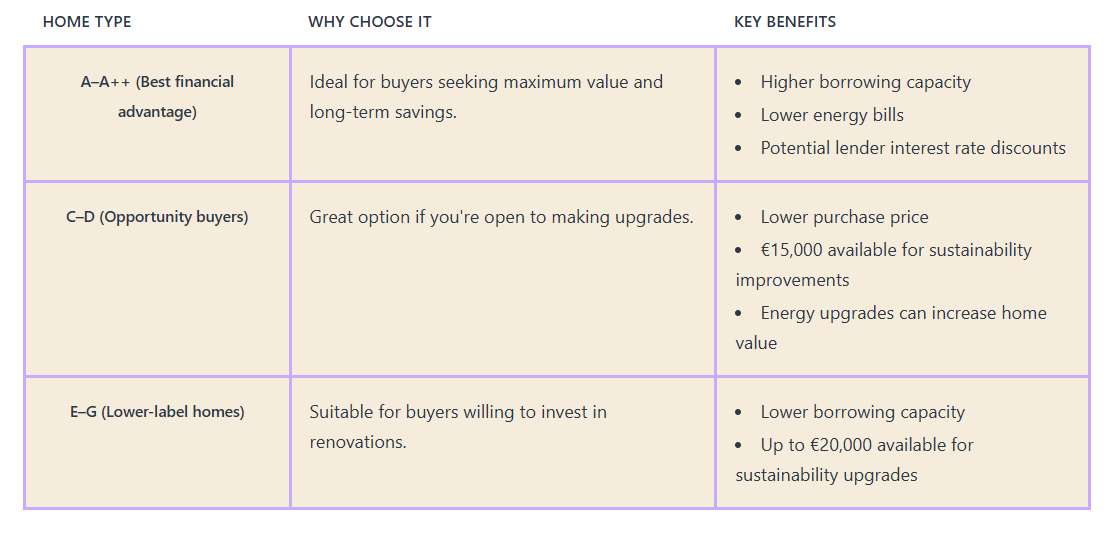

What if your home has a lower energy label?

Homes with lower labels (E–G) bring two financial outcomes:

Lower borrowing capacity.

Up to €20,000 available for sustainability upgrades.

These upgrades can help you transition your home into a more sustainable home with better long-term comfort and value.

Mortgage interest discounts for high energy labels

Some lenders — such as ABN AMRO or ING— offer interest rate discounts if:

You buy a home with a label B or higher, or

You upgrade your home to label B or A within 24 months.

Lower mortgage interest rates mean better affordability and reduced long-term costs. Use our mortgage calculator to check the current market interest rates based on your home’s energy label.

Energy labels now shape your borrowing capacity, renovation budget, and long-term financial planning. Understanding how these rules work helps you make smarter decisions — whether you are buying a highly efficient home or upgrading a lower-label property.

Do you want to learn more and get personalised advice on how much your mortgage could be in the Netherlands? Contact our mortgage advisor for a free, no-obligation consultation.

Our happy clients

We focus on delivering great results — and our clients' feedback tells the rest of the story.