The amount you can borrow for a mortgage in the Netherlands doesn’t depend only on your income or interest rates. Other factors—such as your home’s energy label and expected wage developments—also influence your borrowing capacity. Here’s a summary of the changes coming in 2026 and what they could mean for your mortgage options.

This blog is written by Toni, our mortgage advisor at OHAO, and provides an overview of what you can expect your mortgage borrowing capacity to look like in 2026.

How much mortgage can you borrow in 2026?

Each year, the National Institute for Budget Information (Nibud) publishes calculations showing how much households can borrow. For 2026, Nibud expects an average wage increase of 4.1% in the Netherlands. A salary increase of this size can slightly boost your borrowing capacity.

For income levels up to around €65,000, borrowing power will remain nearly the same as in 2025. From €70,000 and above, the increase becomes more visible. With a €70,000 income, you may be able to borrow about €7,500 more.

For even higher incomes—around €100,000—the increase is larger, with borrowing capacity rising by around €15,500 compared to 2025.

Including a future salary increase

If you know your salary will increase within the next six months, you can often use that higher income in your mortgage application. Your employer will need to confirm the upcoming raise in writing (a letter of consent).

Borrow more with wage increases in 2026

Since salaries are expected to rise by 4.1%, anyone receiving a similar increase may qualify for a higher mortgage next year. The effect depends on your income bracket; however, in general, a higher salary results in a higher maximum mortgage amount.

New changes to the energy label rules in 2026

Since 2024, your home's energy label has played a direct role in how much you can borrow for a mortgage. The idea is simple: if a home is more energy-efficient, you can probably spend less on utilities each month. That means you might be able to borrow more because you’ll have more left over in your budget.

Adjustments to borrowing amounts for high-energy labels

In 2026, the additional borrowing capacity for very energy-efficient homes will be slightly reduced:

A+++ homes

Additional borrowing in 2025: €30,000

Additional borrowing in 2026: €25,000

A++++ homes

Additional borrowing in 2025: €50,000

Additional borrowing in 2026: €40,000

These adjustments are primarily due to reduced financial benefits from solar panels, as feed-in costs rise and the net-metering scheme is set to end in 2027.

Energy label home | Additional mortgage amount |

E, F, G | €0 |

C, D | €5,000 |

A, B | €10,000 |

A+, A++ | €20,000 |

A+++ | €25,000 |

A++++ | €30,000 |

A++++(+) | €40,000 |

Energy label and borrowing for sustainability improvements

In 2024, it was also introduced the new rule which allows both buyers and existing homeowners to borrow extra money specifically for sustainability upgrades. The amount depends on the home’s current energy label.

This additional borrowing is intended to make homes more energy-efficient and reduce long-term energy costs.

Example

If you purchase a home with an energy label C and plan to improve its efficiency, you can borrow up to €15,000 extra for these upgrades. The table below shows how much you can borrow for sustainable improvements in 2026.

Your current energy label | Additional borrowing capacity |

E,F,G | €20,000 |

C,D | €15,000 |

A to A++, B | €10,000 |

A+++ and A++++ | 0 |

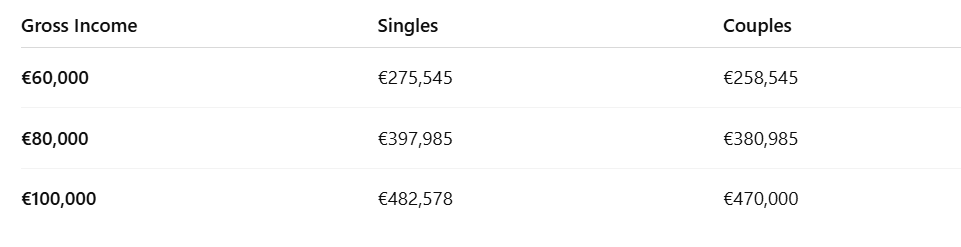

Extra help for single homebuyers in 2026

If you are planning to buy a house by yourself in 2026, there’s some encouraging news: you still be able to borrow up to €17,000 more than usual. This boost is intended to level the playing field for single buyers, as couples with two incomes often have an easier time qualifying for a larger mortgage.

National Mortgage Guarantee (NHG) in 2026

In 2026, the maximum purchase price for a home with an NHG-backed mortgage will be:

€470,000, including renovation costs

€498,200 if the extra amount is fully used for energy-saving measures

Starting in 2026, these NHG limits will apply to all types of housing, including tiny houses, houseboats, and flexible housing solutions. The separate limit for caravans has been removed. The NHG fee will remain the same: 0.4% of the mortgage amount.

If you are considering waiting until 2026 to buy a home, now is a great time to start preparing. Understanding how next year’s rules, income developments, and energy-label updates affect your borrowing capacity can put you in a stronger position when the time comes. Our mortgage advisors can help you explore your options, calculate your maximum mortgage for 2026, and guide you through which rules and benefits apply best to your situation.

Our happy clients

We focus on delivering great results — and our clients' feedback tells the rest of the story.